Simpson Manufacturing reveals its Q3 2024 figures

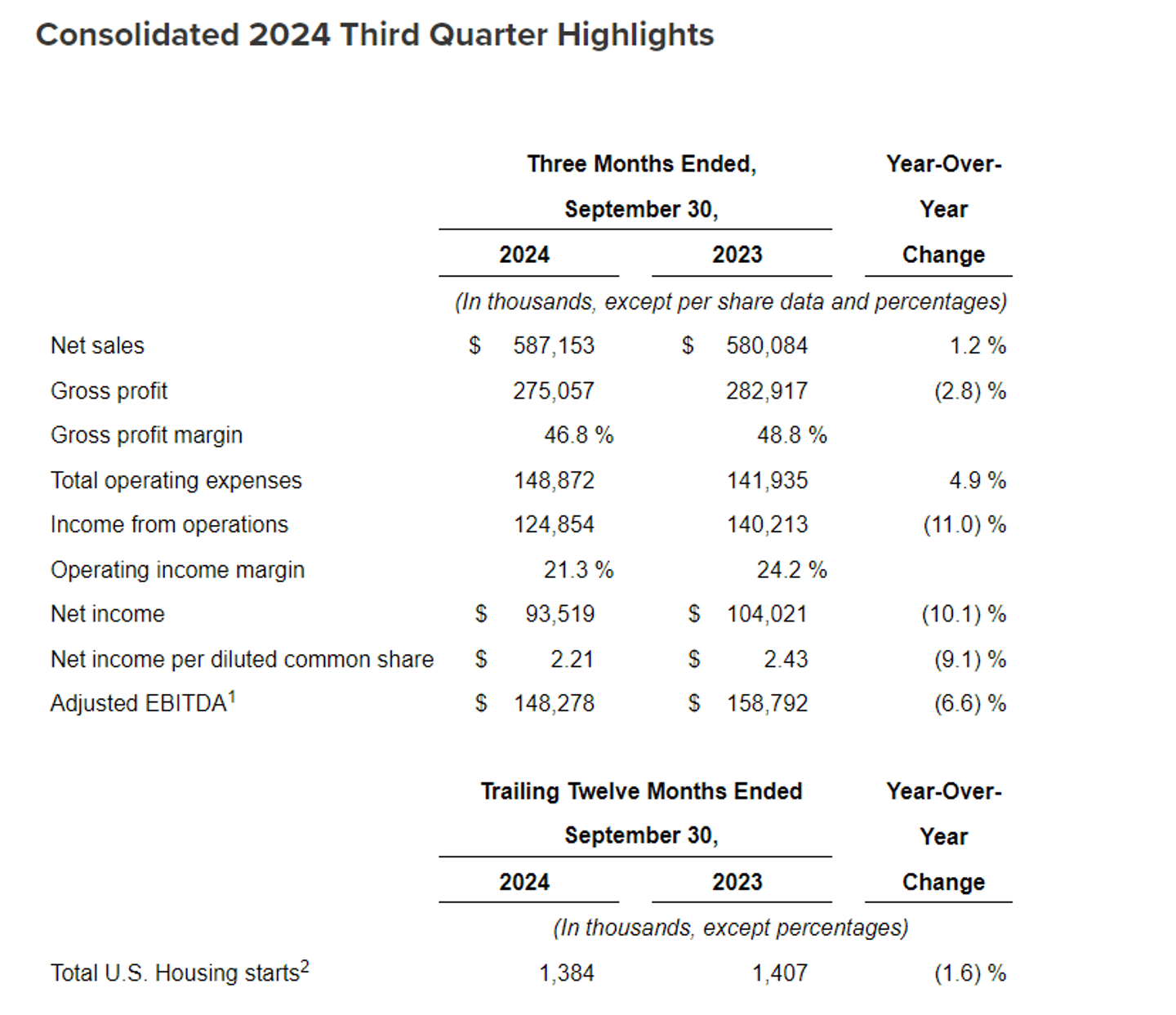

Simpson Manufacturing Co., Inc. has shared its financial results for the third quarter of 2024. All comparisons below refer to the quarter ended September 30, 2024, with the quarter ended September 30, 2023.

North America segment Q3 2024 financial highlights

- Net sales of $461.4 million increased 1 percent from $456.8 million due to slightly higher average sales prices resulting from a favorable sales mix on relatively flat sales volumes, in addition to incremental sales from the company's 2024 acquisitions.

- Gross margin decreased to 49.5 percent from 51.8 percent, primarily due to higher factory and overhead and warehouse costs, as a percentage of net sales, partly offset by efficiency gains.

- Income from operations of $123.3 million decreased 9.1 percent from $135.6 million. The decrease was primarily due to a decrease in gross profit, as well as increases in operating expenses of $4.1 million from 22.1 percent of net sales to 22.7 percent. Increased operating expenses include personnel costs (including engineering support services) and advertising and tradeshow costs, which were partly offset by a decrease in variable incentive compensation.

Corporate developments

During the third quarter, the company completed the acquisition of all of the operating assets and assumed liabilities of Monet DeSauw Inc. and certain properties of Callaway Properties, LLC (together with its subsidiaries, "Monet") for a total purchase consideration of approximately $48.5 million, net of cash received. Monet specializes in the production of large-scale saws and material handling equipment for the truss industry in the U.S.

During the third quarter, the company completed the acquisition of QuickFrames USA, a manufacturer of pre-engineered structural support systems for commercial construction with sales in North America.

Balance sheet & 2024 third quarter cash flow highlights

- As of September 30, 2024, cash and cash equivalents totaled $339.4 million with total debt outstanding of $465.4 million, of which $75.0 million remained outstanding under its $450 million revolving credit facility.

- Cash flow provided by operating activities of $102.5 million decreased from $200.9 million, primarily due to increases in working capital.

- Cash flow used in investing activities of $106.6 million increased from $18.5 million due to increases of $61.5 million in acquisitions and $25.6 million in capital expenditures.

Business outlook

The company has updated its 2024 financial outlook based on three quarters of financial information to reflect its latest expectations regarding demand trends, cost of sales and operating expenses. Based on business trends and conditions as of October 21, 2024, the company's outlook for the full fiscal year ending December 31, 2024 is as follows:

- Based on current expectations that U.S. housing starts will be down from the prior year, operating margin is estimated to be in the range of 19.0 to 19.5 percent.

- Capital expenditures are estimated to be in the range of $175 million to $185 million, which includes $90 million to $100.0 million for the Columbus, Ohio, facility expansion and the new Gallatin, Tennessee, fastener facility construction, with the remaining spend carrying over into 2025.

Management commentary

"Our third quarter net sales of $587.2 million were up modestly year-over-year despite the housing markets in both the U.S. and Europe remaining under pressure," commented Mike Olosky, president and CEO of Simpson Manufacturing Co., Inc.

"In North America, our volumes were relatively flat year-over-year with strength in the national retail, component manufacturer and OEM markets offsetting weakness in residential and commercial. While product mix drove a higher average sales price per pound in the quarter, our customer mix resulted in greater volume discounts applied. In Europe, sales increased modestly year-over-year, outperforming the market as we've continued to benefit from new customer wins and product applications."

Olosky continued: "Despite near-term challenges, we grew our North America volume by 500 basis points ahead of U.S. housing starts over the trailing 12 months. Even though our overall profitability is good, it is below our expectations and we are working to align costs with market conditions to improve profitability. For 2024, we now expect U.S. housing starts to be down in the low single-digit range from 2023 with low single-digit growth to come in 2025. In Europe, 2024 housing starts are expected to be down in the high single-digit range compared to the prior year with meaningful growth to be pushed out further into 2026 and beyond."

Click here for Simpson's full financial data from Q3 2024.