Market Recap: RISI Crow's Construction Materials Cost Index

A price index of lumber and panels used in actual construction for Nov. 3, 2017.

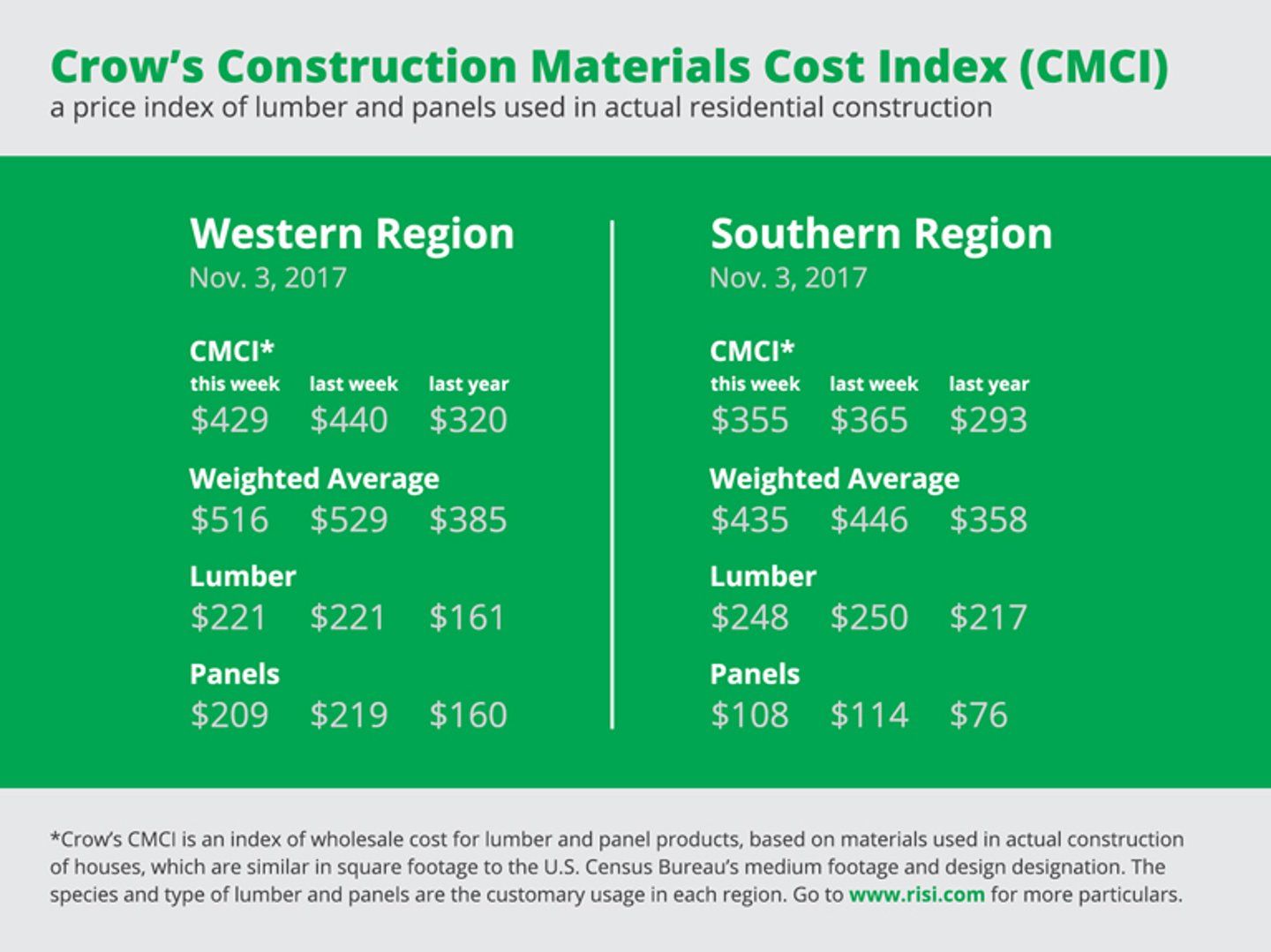

Western: regional species perimeter foundation

Southern: regional species slab construction

Crow's Market Recap: A condensed recap of the market conditions for the major North American softwood lumber and panel products as reported in Crow's Weekly Market Report.

Lumber

SPF lumber prices continued their trek higher for the tenth consecutive week. Mills pushed order files out further, some now selling as far out as mid-December. Market players displayed little surprise in the Commerce department’s affirmative final decision on duties, but some confusion was evident.

Southern Pine discounting across all #1 and #2 items was evident, but the depth of discounts subsided, particularly on the westside. Improved sales volumes beginning early in the week helped mills rid themselves of buildups, prompting traders to describe a market “firming up.”

Dry Coastal species prices managed to hold up while green Doug Fir #2&Btr discounts were found across all dimensions. Some producers were willing to discount dry Doug Fir items a few dollars to keep wood moving, while others held onto prices more firmly.

Some solid gains were registered in Inland species #2&Btr, and very good increases showed up in Select Structural and MSR lumber. Demand continues to extend mill order files, most of which are three weeks or more in #2&Btr. Some MSR producers are out almost a month now on both 2x4 and 2x6.

Stud prices remained mixed, with price direction depending on the item and species. SPF producers reported improved 2x4 8’ sales activity, helping to limit downward moves for that item and generate some firmer quotes.

Radiata Pine is still readily available.

In Ponderosa Pine, little mention was made in reports with regard to Mldg&Btr, but it shows some tightness. Buyers are finding it difficult to source 5/4 #2 Shop, resulting in a $10 gain for that item. Ponderosa Pine Selects are stable and steady in their movement. All Ponderosa Common boards continue to be in reasonable demand, with supplies at mill level still being tested.

Western Red Cedar purchases were often concentrated on filling in inventories with minimal volumes of several items. Overall, sales activity was seasonally modest as the calendar flipped to November.

Panels

Pricing for OSB is now coming off in chunks, as the market makes a correction after a meteoric rise accelerated by hurricanes. Buyers are exceedingly wary, and mills are taking discounts to move order files out. As a result, pricing is all over the map through most of North America.

Southern Pine rated sheathing discounts grew deeper, with the biggest cuts occurring in thicker panels. A slower sales pace forced producers to lower prices in an attempt to sell off panels available in the week of November 6. By Friday, mills extended order files into Nov. 13.

Western Fir sheathing prices continued to adjust lower, as mills tried to sell more aggressively to customers not wanting to participate in a weakening market. Those buyers needing to purchase found prompt availability for some items and significant volumes for shipment the week of Nov. 6.

Canadian plywood markets reached what sources agree is a comfortable stabilization this week, and buyers came back to the table in greater numbers. Price deterioration halted, giving renewed confidence to players.

Sales of both particleboard and MDF were lackluster. Yards kept close check on inventories, with some paring back those levels prior to the year’s end.

For more on RISI, click here.