Market Recap: RISI Crow's Construction Materials Cost Index

A price index of lumber and panels used in actual construction for April 26, 2013

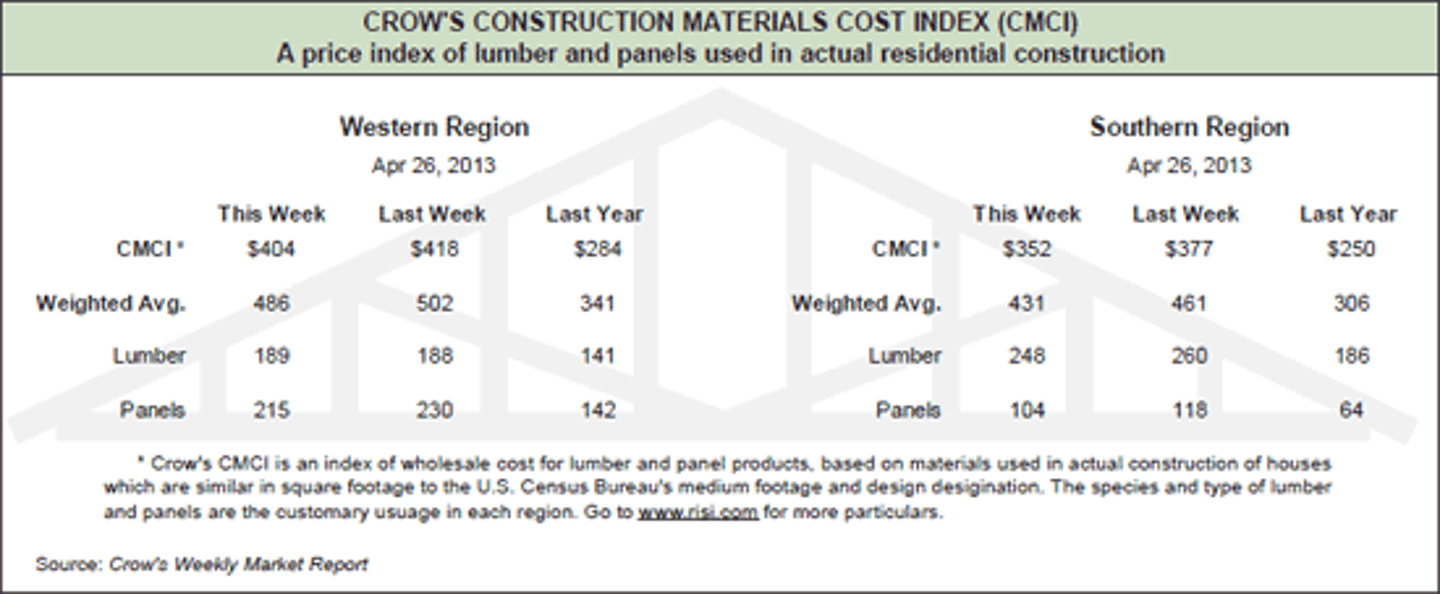

*Western - regional species perimeter foundation; Southern - regional species slab construction.

Crow's Market Recap -- A condensed recap of the market conditions for the major North American softwood lumber and panel products as reported in Crow's Weekly Market Report.

Lumber: SPF lumber prices continued to drop, in many instances by double digits, as producers across Canada tried to find price levels that would draw more interest from buyers. Producers reported improved demand at the lower price levels. Southern Pine lumber producers sold prompt shipping volumes in some instances at discounts of $30 to $40 in an effort to control growing floor stocks of particular items. Where selling floor stocks was not as pressing, mills discounted less, willing to stack more lumber until prices rebound. Coastal species lumber mills became more aggressive in their approach, forcing market prices down in bigger chunks. The need to sell production varied, generating a broad range of mill quotes and selling levels. Price concessions and prompt shipments were the keys to successful sales for Inland species lumber. Even so, sales volumes remained light, as buyers remained on the sidelines. Light sales of Radiata Pine Mldg&Btr continued, as asking prices put it out of buyers' reach in many cases. Sales of Ponderosa Pine Moulding and Shop lumber remained active, in spite of little participation from window plants. Limited supplies of Shop grades added to the market's strength. Sales activity for Ponderosa Pine boards was quiet. Buyers remained on the sidelines, especially when it came to #2. Eastern White Pine producers reported steady demand and sales for Industrial. Select sales remained slow. Activity for ESLP was quiet as buyers remained on the sidelines. Western Red Cedar producers continued to sell moderate volumes at a steady pace, leaving prices very firm or edging higher. Producers catering to home center outlets generally reported better sales to those stores than to wholesalers and retailers.

Panels: OSB prices often changed several times in a day, as both producers and buyers searched for a trading level. The late arrival of spring was blamed for the market weakness, along with limited available credit and increased production. Slow trading left the Southern Pine plywood market quieter than it has been in weeks. Mill order files extending out into the middle of May allowed producers to hold prices while wholesalers discounted. Western Fir plywood mills aggressively lowered prices and accepted counters to move order files beyond a certain point. Buyers willing to purchase significant volumes took advantage of CDX items at levels discounted $30 to $40. After a quiet start, Canadian plywood buyers came to producers with offers that fit mills' needs. The sales allowed producers to extend their order files into the middle of May and hold a better line on discounts. Western particleboard producers continued to experience varying degrees of improvement in their market. MDF sales in both the East and West remained strong.

For more on RISI, click here.