Are starter homes becoming more affordable?

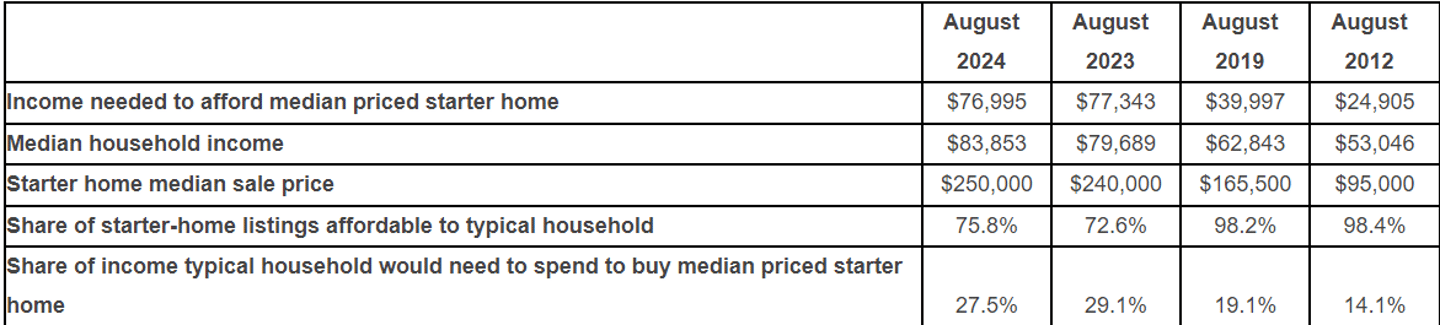

U.S. homebuyers need to earn $76,995 per year to afford the median priced starter home ($250,000), which is down 0.4 percent year over year, according to a new report from real estate brokerage Redfin.

That’s the first annual decline since August 2020, when mortgage rates were nearing their record low.

Starter-home prices are up 4.2 percent year over year, but the income needed to afford a starter home fell because mortgage rates dropped enough to offset the increase in prices. The average interest rate on a 30-year mortgage fell to 6.5 percent in August from 7.07 percent a year earlier, the first annual decrease in three years. It has since declined further, now sitting at 6.08 percent. Still, the income needed to afford a starter home is only 3.6 percent below the record high of $79,857 hit last fall, per Redfin.

“It’s great news that starter homes are becoming a little more affordable, but there’s a catch,” said Redfin Senior Economist Elijah de la Campa. “Starter homes aren’t what they used to be. A decade ago, a turnkey four-bedroom house in a nice neighborhood was often considered a starter home, but today, a small fixer-upper condo is often all a first-time homebuyer can afford. The American Dream is changing; for many, it no longer involves a house and a white picket fence.”

House hunters should be aware that starter-home affordability may not improve much more, if at all, in the near future. The Federal Reserve’s latest interest rate cut and its plans for future cuts were highly anticipated, meaning they’re mostly priced into mortgage rates already. When the Fed cuts short-term interest rates, long-term rates like mortgage rates don't always move down nearly as much. Home prices also tend to rise over time, so waiting to buy likely means a higher price tag and down payment.

Both Kamala Harris and Donald Trump have said they want to make homes more affordable, so buyers may get more clarity on how the next president will tackle the housing affordability crisis come November.

Starter homes are much less affordable than they were before the pandemic

The typical household earns an estimated $83,853 per year, which is 8.9 percent more than they need to afford the median priced starter home. That’s an improvement from last August, when the typical household only earned 3 percent more than they needed. But it’s a setback from before the pandemic; in August 2019, the typical household earned 57.1 percent more than they needed to afford the median priced starter home, and in August 2012, they earned 113 percent more, or over twice as much as they needed.

Housing prices skyrocketed during the pandemic home buying frenzy as a severe shortage of homes for sale coincided with a surge in demand that was fueled by record-low mortgage rates. Starter-home prices are now 51.1 percent higher than they were in August 2019 and 163 percent higher than they were in August 2012. Home prices have risen much faster than incomes, which are now 33.4 percent higher than they were in 2019 and 58.1 percent higher than they were in 2012. Put another way, the income needed to afford a starter home has tripled since 2012, while the median household income hasn’t even doubled.

Three-quarters (75.8 percent) of starter-home listings are affordable for a household making the median income. While that’s up from 72.6 percent last August, it’s down from nearly 100 percent in both 2019 and 2012. Of course, not everyone buying a starter home actually earns the median income; a household earning 80 percent of the median income would only be able to afford 43.1 percent of listings.

“While many people make enough on paper to afford a starter home, they often have other expenses like student debt that are preventing them from buying,” said Blakely Minton, a real estate agent in Philadelphia.

“Starter-home buyers are skewing older than they used to. When I first started working in real estate 20 years ago, they were kids fresh out of college. Now grads are saddled with huge student loans and are moving back in with Mom and Dad or renting,” Minton said. “I bought my first house at 23, but that’s hard to do today, in part because first-time buyers are competing with older Americans who want to downsize and are able to make higher offers.”

A household on the median income would need to spend 27.5 percent of their earnings on housing to buy the median priced starter home, down from 29.1 percent last summer. That means the typical household would not be “cost burdened” if they purchased the typical starter home because they’d be spending less than 30 percent of their income on housing. But they’re more likely to be cost burdened than in the past; a median-earning household would’ve needed to spend less than 20% of their earnings to buy the typical starter home in both 2019 and 2012.

A household earning only 80 percent of the median income would have to spend 34.4% of their earnings on housing to buy the median priced starter home, meaning they would be cost burdened.

Pandemic boomtowns see steepest drops in income needed to afford a starter home

In Anaheim, Calif., homebuyers need to earn an annual income of $217,300 to afford the median priced starter home, down 8.1 percent year over year—the largest decline among the 50 most populous U.S. metropolitan areas. Next came Austin, Texas (-5.8%), West Palm Beach, Fla. (-5%), Phoenix (-4.8%) and Dallas (-4.7%).

Home prices in many of the aforementioned metros soared during the pandemic as scores of out-of-towners moved in, but are now coming back down to earth. Starter-home prices in Austin are down 3 percent year over year—more than any other major metro. West Palm Beach and Dallas also saw declines.

It’s worth noting that Anaheim remains one of the least affordable metros in the nation, with less than 0.1 percent of starter-home listings affordable for a household earning the median income.

In four metros, starter homes went from unaffordable in 2023 to affordable in 2024

There were four metros where starter homes went from unaffordable in 2023 to affordable in 2024, meaning a household on the median income would now need to spend less than 30 percent of their earnings to buy the typical starter home. All four metros are in Florida or Texas, which have recently seen their housing markets soften amid surging housing supply and intensifying climate risk.

In West Palm Beach, a household on the median income would now need to spend 28 percent of their earnings on housing to buy the median priced starter home, down from 31 percent last August. Fort Lauderdale went to 28.2 percent from 30.9 percent, while Dallas went to 29.1 percent from 32.1 percent and Fort Worth went to 28.3 percent from 30.2 percent.

The Midwest is home to three of five metros with biggest increases in income needed to afford a home

In Chicago, homebuyers need to earn an annual income of $77,238 to afford the median priced starter home, up 15.4 percent year over year—the steepest increase among the metros Redfin analyzed. Next came Los Angeles (14.7 percent), Detroit (14.5 percent), Cincinnati (9.7 percent) and Pittsburgh (9.6 percent).

These metros have seen some of the biggest jumps in home prices, which is driving up the income needed to afford a home. Starter-home prices in Detroit jumped 22.8 percent year over year in August—a bigger increase than any other major metro. Next came Pittsburgh (18.4 percent) and Cincinnati (15.6 percent). Chicago and Los Angeles also saw above-average increases.

Many homebuyers have flocked to the Midwest in recent years because it’s known to be more affordable. That influx of demand has helped push up home prices.

To view Redfin's full report, including charts, click here.